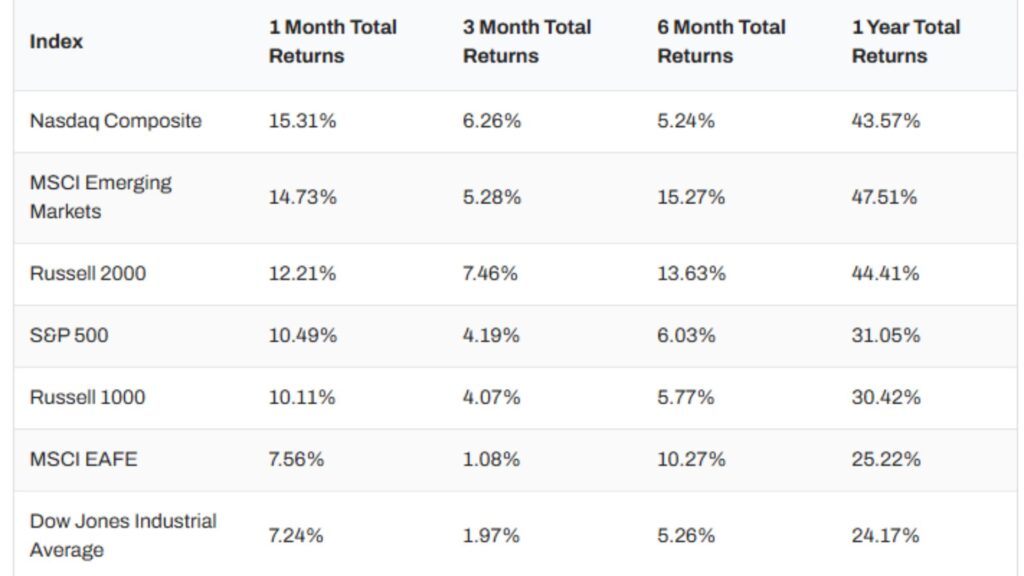

April Market Wrap – A Powerful Rebound

April was one of those sharp snapback months—in a good way. The S&P 500 jumped 10.5%, its strongest showing since late 2020, while the Nasdaq Composite led the charge with a 15.3% gain. Broadly speaking, this wasn’t a narrow rally—five major indices cleared double-digit returns, which tells you the move had real breadth behind it.

Under the hood, though, it wasn’t evenly distributed. Tech absolutely stole the show, ripping more than 20%, while Real Estate put in a solid but more modest 8.7%. Energy, which had been hot in March, cooled off—down 2.6%—as uncertainty around Iran kept that trade choppy rather than trending.

What makes the move more interesting is the context. We came into April off a pretty rough Q1, with the market down over 7% at one point and sentiment scraping the bottom. That set the stage for a classic positioning unwind. Starting March 31, the S&P strung together seven straight up days, effectively clawing back the entire quarter’s losses and kicking off the momentum that carried through April.

From a tape perspective, it was impressively steady. Out of 21 trading days, the S&P finished green 15 times—about 71%—and never dropped more than 0.5% in a single session. That kind of low-vol, grind-up move is exactly what you’d expect in a market increasingly driven by systematic flows and fast information loops.

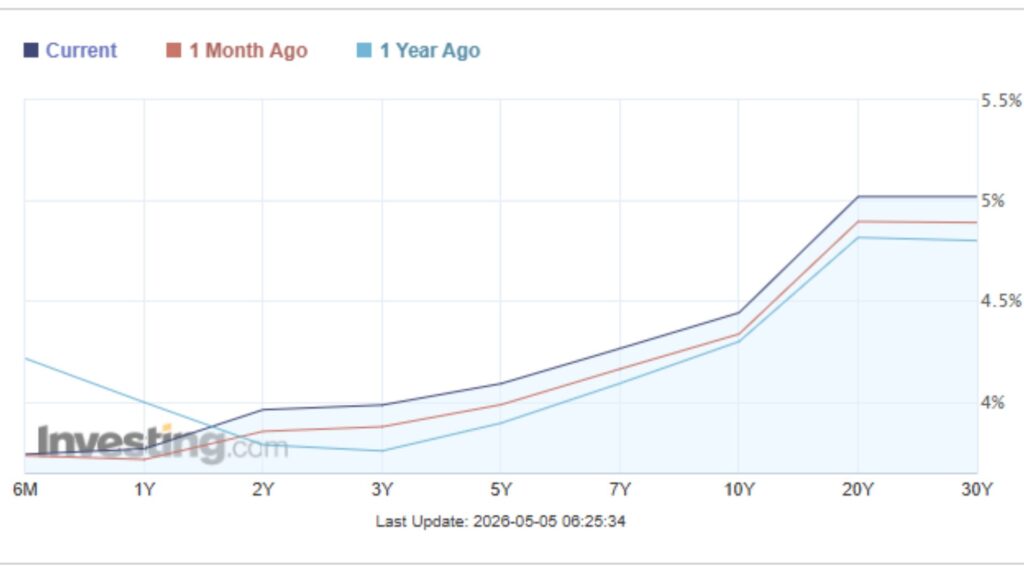

Fixed Income & Treasury Yields

Month-over-month, the yield curve has shifted modestly higher and slightly steeper, with rates across most maturities ticking up—most notably in the intermediate to long end (10Y–30Y). Short-term yields remain relatively anchored, suggesting the market is still pricing a steady policy stance from the Federal Reserve, while the rise further out reflects firmer growth and inflation expectations. Overall, it’s a subtle but important move toward a more “normal” upward-sloping curve.

Macro & Commodity Update

Macro didn’t get in the way. The Federal Reserve remains in wait-and-see mode, with the next meeting on June 17 and rate-cut expectations still basically negligible—sub-5%. Labor data came in stronger than expected, with 178,000 jobs added and unemployment ticking down to 4.3%, which reinforces the “no rush to cut” narrative.

Inflation surprised a bit on the upside, with headline CPI up 0.9% month-over-month to 3.3% (the biggest jump since 2021), though core inflation stayed relatively contained at 2.6%.

Commodities were mixed. Gold pulled back about 1%, with the SPDR Gold Shares ETF (GLD) ending around $423.66, and silver lagged slightly more, down 2.1%. Oil, on the other hand, remained the headline story—geopolitics did the heavy lifting there. Tensions involving Iran pushed Brent up to ~$113.89 and WTI close to $100, keeping U.S. gas prices stubbornly above $4/gallon.

Crypto kept its momentum going for a second straight month. Bitcoin rallied 13.6% to around $75.8k, and Ethereum added 11.4% to roughly $2.25k—risk appetite clearly isn’t confined to equities.

Market Outlook – Reality Check Ahead

April was a textbook snapback rally fueled by positioning, momentum, and resilient macro data. The question now is whether this leg higher has real fundamental follow-through—or if we’ve just pulled forward returns in a market that’s still very headline-driven.

May looks more like a digestion phase than a continuation of the rally. The S&P 500 is entering the month with strong momentum but stretched positioning, and the focus is shifting back to fundamentals. The Federal Reserve remains firmly in “higher for longer” mode, with inflation still sticky and the labor market holding up. That backdrop limits multiple expansion, especially for tech, which led April’s gains and now carries elevated expectations. As a result, the market is likely to trade more sideways, with increased volatility and sector rotation rather than broad-based upside.

The key variables for May will be inflation data, earnings guidance, and energy prices—particularly with geopolitical tensions involving Iran keeping oil elevated. Any upside surprises in inflation or signs of slowing earnings could trigger a pullback after April’s rapid run.

Bottom line: the rally needs validation from fundamentals, and until that shows up, a choppier, more selective market environment is the most likely path forward.