February Market Wrap — Stability on the Surface, Rotation Beneath

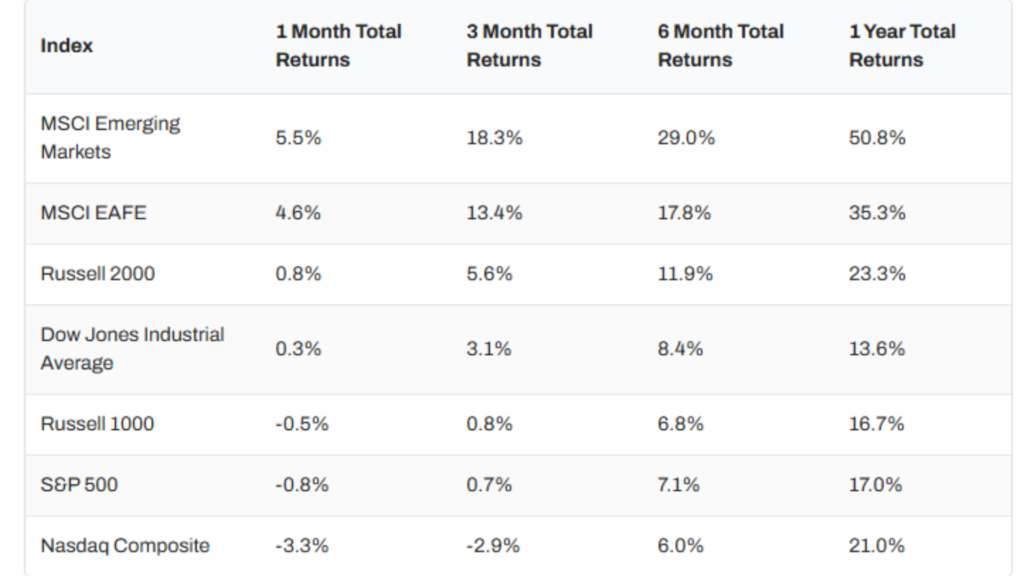

February delivered a mixed bag for markets, with international equities once again taking the top spot. Emerging markets led the charge, climbing 5.5% for the month, while the S&P 500 slipped 0.8%. Tech continued to struggle— the Nasdaq logged its second straight month as the weakest major index, falling 3.3%.

Under the surface in the US market, sector performance was notably uneven. Defensive and commodity-linked areas stood out: Utilities surged 10.4% and Energy gained 9.5%. On the other end, four sectors closed the month in the red, with Financials lagging for the second consecutive month, down 3.8%.

Fixed Income & Treasury Yields

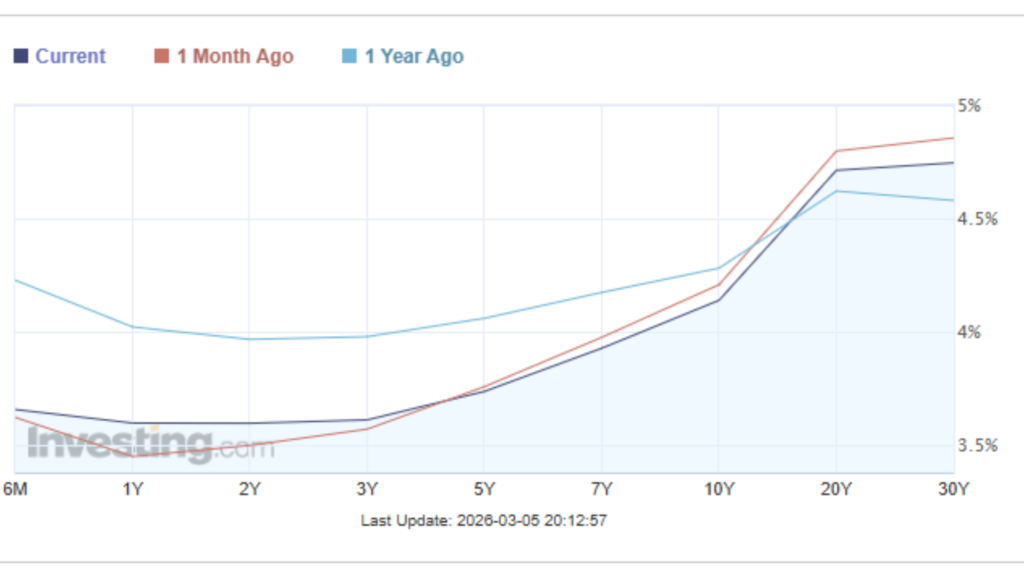

The Treasury yield curve shifted notably lower in February, reflecting a broad decline in longer-term yields even as the very short end remained relatively stable. Intermediate maturities such as the 3- and 5-year Treasuries were stable, while the 10-year posted the largest drop of the month. Longer-dated bonds followed a similar pattern, with the 20- and 30-year yields each declining by more than 20 basis points.

Overall, the curve became slightly flatter at the short end while long-term yields fell more sharply, reflecting stronger demand for duration and growing expectations that policy rates may ease later in the cycle.

AI Drives a Reset Across Software Valuations

February exposed a growing divergence beneath the market’s surface. While the S&P 500 appeared relatively stable, software stocks experienced a sharp pullback, underscoring renewed pressure across the SaaS landscape. The rapid expansion of AI has intensified investor scrutiny around the long-term defensibility of many software business models. As a result, investors are increasingly distinguishing between platforms that can successfully integrate AI and those that may face margin pressure or potential disruption.

Importantly, this move did not reflect a collapse in fundamentals, but rather a reset in expectations. Revenue and earnings trends across much of the industry remained intact. However, valuations had been stretched and priced for near-flawless execution, so even modest adjustments to guidance helped accelerate the repricing.

For investors, the divergence serves as a useful reminder of how quickly leadership can shift when sentiment changes. February reinforced a key theme for 2026: broad index stability can often mask significant internal rotation, making thoughtful positioning increasingly important.

Macro and Commodity Update

Inflation continued trending in the right direction to start the year. The U.S. inflation rate eased to 2.40% in January, moving closer to the Federal Reserve’s 2% target, though core inflation ticked higher to 3.09%. According to the CME FedWatch tool, markets are pricing in less than a 3% probability of the first rate cut of 2026 at the FOMC’s upcoming March 18 meeting. The Fed held rates steady at 3.50–3.75% in January, marking the first pause in cuts since September.

Precious metals delivered another strong month. Gold surged 7.93%, pushing the SPDR Gold Shares ETF (GLD) to $483.75 per share. Silver experienced a more volatile stretch but ultimately finished February with an impressive 12.66% gain.

Energy markets were relatively stable despite ongoing geopolitical tensions. Brent crude slipped 0.48% to $71.90 per barrel, while WTI crude moved higher, gaining 2.88% to $66.36.

Cryptocurrencies, however, remained under pressure. Bitcoin declined for the fifth consecutive month, falling 21.7% to $65,883.99. Ethereum saw an even steeper pullback, dropping 28.5% to $1,931.32. Since the start of 2025, Bitcoin and Ethereum are now down 28.9% and 42.5%, respectively.

Geopolitical Tensions: The War in Iran

Geopolitical risk also moved back to the forefront as conflict in the Middle East escalated following the outbreak of war involving Iran, the United States, and Israel. Since late February, a series of airstrikes and retaliatory missile and drone attacks have spread across the region, with targets including military facilities in Iran as well as U.S. bases and allied infrastructure throughout the Persian Gulf.

The conflict has already begun to affect global markets. Energy supply routes—particularly around the Strait of Hormuz—have faced disruption risks, contributing to volatility in oil prices and shipping activity. While markets have so far absorbed the news without widespread panic, investors remain sensitive to the possibility of a broader regional escalation that could impact energy markets, inflation expectations, and overall global growth.

For now, geopolitical developments remain a key risk factor to monitor as markets move through March, particularly given the potential for further volatility in commodities and global trade flows.

Market Outlook

As markets enter March, investors remain focused on monetary policy, economic momentum, and rising geopolitical risks. February’s decline in Treasury yields and continued progress on inflation suggest financial conditions may gradually ease, though expectations for a near-term rate cut remain very low ahead of the Federal Reserve’s March 18 meeting.

Within equities, sector rotation remains a key theme. February showed how stable index performance can mask meaningful divergences beneath the surface, particularly as software stocks repriced amid growing scrutiny around AI-driven competition.

Investors are also closely monitoring the war in the Middle East, particularly developments involving Iran, as the conflict has the potential to impact global energy markets and inflation expectations. While markets have remained relatively resilient so far, geopolitical developments could introduce additional volatility in the weeks ahead.