May Market Wrap – Broad Gains, Tech in Front

May picked up right where April left off — green across the board. Every major index we track finished higher, with Emerging Markets leading the pack at 9.71% and the S&P 500 tacking on another 5.26%. This wasn’t a one-index story, either: all seven of the majors we follow cleared at least 2.9%, so the move had real breadth behind it.

Under the hood, though, it was anything but even. Technology absolutely ran the table — up roughly 20% for a second straight month and accounting for all ten of the S&P 500’s top performers. Energy, meanwhile, stayed in the penalty box, down about 5.6% as the on-again, off-again U.S.–Iran situation kept that trade jumpy rather than trending.

The context makes the run more impressive. April had already delivered the S&P’s best month since late 2020, so the easy assumption was that May would cool off. Instead, momentum carried straight through — and the index pushed to fresh record highs as June got underway. There was even a changing of the guard at the Fed mid-month: Jerome Powell wrapped up eight years as Chair on May 15, handing the gavel to Kevin Warsh, and the market barely blinked.

From a tape perspective, it was another steady grind. The S&P closed out May riding an eight-session winning streak — its longest in about a year — the kind of low-drama, climb-the-wall move you tend to see when systematic flows and AI optimism are doing the driving.

| Index | 1 Month Total Returns | 3 Month Total Returns | 6 Month Total Returns | 1 Year Total Returns |

| MSCI Emerging Markets | 9.71% | 9.47% | 29.54% | 55.15% |

| Nasdaq Composite | 8.43% | 19.19% | 15.79% | 41.98% |

| S&P 500 | 5.26% | 10.52% | 11.34% | 29.78% |

| Russell 1000 | 5.10% | 9.97% | 10.89% | 28.85% |

| Russell 2000 | 4.37% | 11.26% | 17.47% | 43.08% |

| MSCI EAFE | 3.18% | -0.33% | 13.05% | 23.37% |

| Dow Jones Industrial Average | 2.94% | 4.64% | 7.84% | 22.71% |

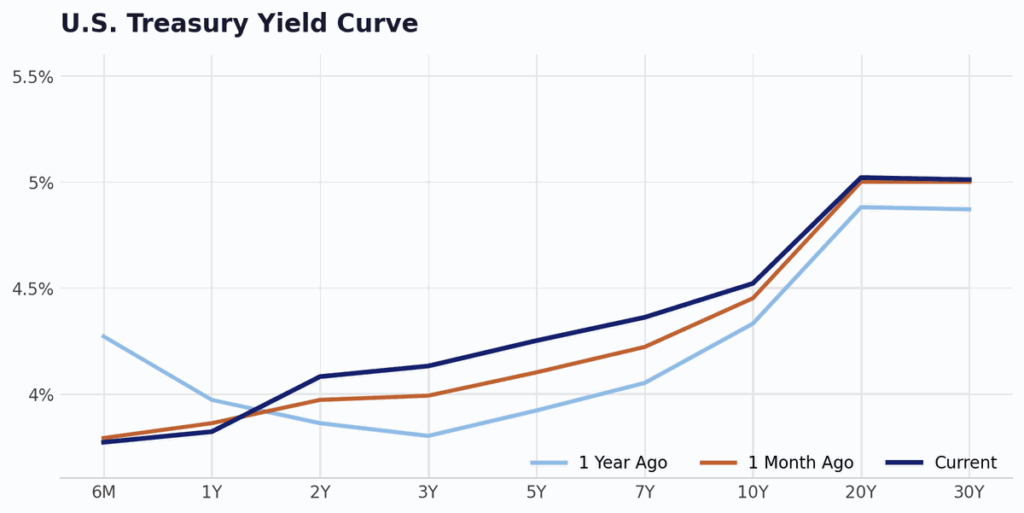

Fixed Income & Treasury Yields

Treasury yields drifted modestly higher across the curve in May, nudging it a touch steeper. The short end stayed relatively anchored — markets are still pricing a steady Fed — while the belly and long end (10Y–30Y) did most of the moving, a subtle nod to firmer growth and sticky inflation. Net-net, it’s a small step toward a more “normal,” upward-sloping curve. The chart below stacks today’s curve against where it sat a month and a year ago.

Macro & Commodity Update

Macro stayed out of the way — mostly. The Fed remains in wait-and-see mode, with the next meeting on June 17 and rate-cut odds still negligible (markets put better than a 99% chance on a hold). The labor market did its part too: employers added 115,000 jobs, comfortably ahead of expectations, and unemployment held at 4.3%.

Inflation is the part worth watching. Headline CPI rose 0.5% on the month to 3.8% — the hottest reading in about two years — though core stayed more contained at 2.8%. Wholesale prices (PPI) ran hotter still at 6.0% year-over-year, a reminder that the last mile on inflation is proving stubborn.

Commodities were a mixed bag. Gold slipped about 1.5% (GLD ended near $410.80) and silver bounced 2.5%. Oil was the headline act again, but in the other direction: a fragile U.S.–Iran ceasefire framework pulled crude well off its April highs, with Brent around $102.75 and WTI near $97.63 — though drivers still felt it with gas above $4.50 a gallon. Crypto took a breather after two strong months, with Bitcoin easing 2.7% to roughly $73.8k and Ethereum down a sharper 10.4% to about $2.0k.

Market Outlook – Momentum Meets the Fed

May was a continuation of April’s momentum — broad, steady, and increasingly led by tech and AI. The question heading into June is whether the fundamentals can validate a market trading at record highs and stretched valuations.

Two events will set the tone. First, the May CPI report on June 10; then the Fed’s June 17 decision — the first under new Chair Kevin Warsh. Markets overwhelmingly expect a hold at 3.50–3.75%, but a soft inflation print could crack the door open to a cut later this summer, something firms like Bank of America are already penciling in. Just as plausibly, another firm reading keeps “higher for longer” firmly in place.

The bigger picture is constructive, with caveats. Wall Street’s 2026 targets lean optimistic — Oppenheimer sees the S&P near 8,100, Morgan Stanley points to strong earnings growth, and AI capex remains the market’s defining theme. But valuations are rich, inflation is sticky, and the labor market is cooling at the edges. That argues for more rotation and the occasional air pocket rather than a straight line higher.

One more thing on the horizon worth flagging: 2026 is shaping up to be a landmark year for IPOs, and three of the most anticipated names are now in motion. SpaceX is leading the charge with a listing expected around June 12 — reportedly targeting a roughly $1.75 trillion valuation and a raise near $75 billion, which would eclipse Saudi Aramco as the largest IPO ever. On the AI side, OpenAI is aiming to go public as early as September, while Anthropic — fresh off a raise at close to a $965 billion valuation — has confidentially filed and is targeting a debut as soon as October at around a $900 billion valuation. Together these deals could pull north of $200 billion from public markets and command combined valuations near $3.6 trillion. For investors, they will be a real test of appetite for richly valued, AI-driven growth — and how they price could tell us a lot about whether the market’s enthusiasm still has room to run.

Bottom line: the trend is your friend, but it needs fundamentals to back it up. Until they do, staying invested, diversified, and a little selective is the smart way to play it.