Stocks Soar Closes H1 with a V-Shaped Rally and Tech Rebound (June 2025)

Market Commentary

June closed out the first half of 2025 on a high note. Equities ripped higher, clawing their way out of earlier-year correction territory: the Dow jumped 4.5%, the S&P 500 gained 6.2%, and the Nasdaq led the pack with a 5.9% advance.

Technology was the clear standout once again—eight of June’s top-10 S&P performers call themselves Information Technology companies, with semiconductors and hardware & storage names doing the heavy lifting. On the flip side, Consumer Staples was the lone laggard, slipping 1.6%, while Technology (+9.9%), Consumer Discretionary (+7.3%) and Energy (+4.9%) rounded out the month’s best-performing sectors.

2025 Midyear Recap

We’re now midway through 2025, and equity markets have absolutely lived up to the “wild ride” tag. After back-to-back banner years, U.S. benchmarks kicked off January with modest gains—Dow, S&P 500, and Nasdaq all inching higher. But by April, a perfect storm of fresh trade tariffs (especially on China), mounting rhetoric, and even spillover unrest in the Middle East drove investors into the safety of short-term Treasuries. The result? Double-digit percentage drops across the board, with the Nasdaq briefly tumbling into bear-market territory.

Then came May’s game changer: a 90-day tariff de-escalation deal that paused some of the steepest levies. Markets took it as a green light to press “go,” and what followed was textbook V-shaped strength. By the end of June, all three major indices were not just clawing back losses but carving out fresh all-time highs—a remarkable turnaround in just six weeks.

Digging into the numbers, the S&P 500 closed H1 up 6.2%, led by Communication Services (+12.1%) and Industrials (+12.0%). Information Technology—after plunging a jaw-dropping 22.7% YTD through April 8—staged the biggest reversal, finishing the first half up 8.9%. Small caps didn’t sit this one out, either: the Russell 2000 snapped back strongly alongside the Dow, underscoring that risk-on sentiment was broadly felt.

It wasn’t all smooth sailing in bonds, though. Tariff jitters, shifting Fed signals, and sticky inflation data kept Treasury yields ping-ponging, reminding us that even “safe” assets can feel anything but safe when geopolitics and price pressures collide.

All told, Q2 drove home two big takeaways: headline risk still dominates headlines—but a well-diversified playbook can turn knee-jerk volatility into a springboard for fresh gains once the headlines calm down.

Fixed Income, Inflation, Earnings Update

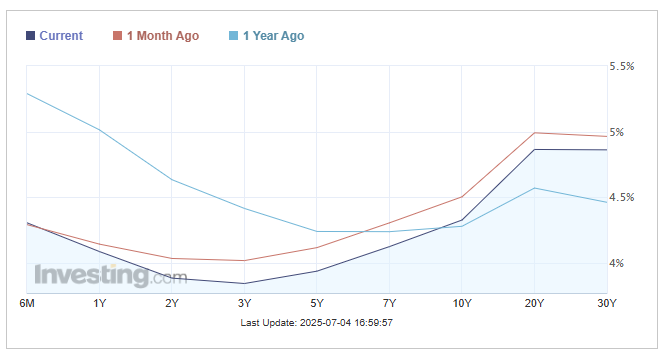

The Fed hit the pause button at its June 18 meeting, keeping the Fed Funds target at 4.25–4.50% for the fourth straight gathering. Rather than rock the boat with another rate hike, the Fed hit pause, balancing its inflation-fighting mandate against the risk of tipping the economy into a slowdown.

Across the Treasury curve, yields were mostly in retreat—every bucket fell by about 17–19 basis points except the 3-month, which ticked up 5 basis points. That decline in rates gave bond funds a boost, with the iShares 20+ Year Treasury ETF (TLT) jumping roughly 2.7% on the month.

Inflation didn’t spike as dramatically as some feared when tariffs kicked in, but prices still felt a bit stubborn. Both the CPI and the Fed’s preferred PCE measure have been inching down, which has eased some of the panic from earlier in the year—though both gauges remain above that 2 percent sweet spot.

On the corporate front, Q1 earnings hit record highs, and while most analysts were bracing for a Q2 growth slowdown, early reports have actually held up pretty well—enough to keep a cautious smile on investors’ faces. In the jobs market, things cooled off a bit: payroll gains slowed, the unemployment rate ticked up to 4.2 percent, and both new and continued unemployment claims trended higher through the quarter.

Asset Class Update

Oil had a wild ride, rallying as much as 25% amid fresh Middle East jitters over Israel-Iran output concerns.

Gold bounced around before settling slightly higher, with GLD up about 0.4% to $308.43.

Meanwhile, new single-family home sales plunged by their biggest monthly margin in three years, though existing home sales eked out a 0.8% gain and the median resale price climbed to within 1% of its all-time high.

Bitcoin finished June up 4.2% at $108,396.60—good for a 17% gain YTD.

Market Outlook

As we roll into the back half of 2025, the S&P 500 is perched just shy of record highs after a roller-coaster first six months. Even with tariff headlines and geopolitical flare-ups trying to steal the show, the U.S. economy has held up surprisingly well—price pressures are cooling, jobless claims are still low, and most economists reckon a recession won’t materialize anytime soon.

Corporate profits got off to a flying start with double-digit Q1 gains, and while analysts are penciling in roughly 5 percent year-over-year growth for Q2, plenty of companies have already signaled upbeat guidance—so don’t be shocked if earnings surprises continue to surprise on the upside.

The Fed, having paused its hiking cycle at a 4.25–4.50 percent policy rate, is telegraphing a few small cuts by year-end, and the futures market is hanging its hat on about three reductions. If the central bank proves more cautious than markets expect, we could see a bit of chop—but on balance, easier money should grease the wheels for stocks.

That said, keep an eye on the usual suspects. The 90-day tariff truce expires in July, so any renewed trade skirmishes—or, better yet, fresh deal-making—will move the needle. Even though spring rollbacks took some of the sting out of top-line duties, a handful of sector-specific levies (think semis or pharma) could still spring up and rattle those corners of the market.

Meanwhile, simmering conflicts in the Middle East haven’t yet sent oil prices through the roof, but a serious escalation would be a quick reminder that no one likes a surprise in their gasoline bill.

On the bright side, the breadth of this year’s rally is widening—industrials, utilities and even a few under-the-radar consumer names are finally tagging along—and that broader participation is exactly what you want to see when markets climb.

Valuations are a bit lofty, so margin for error is thin, but barring any fresh shocks, a diversified lineup of quality growth and select value plays should be set to grind modestly higher into year-end.